|

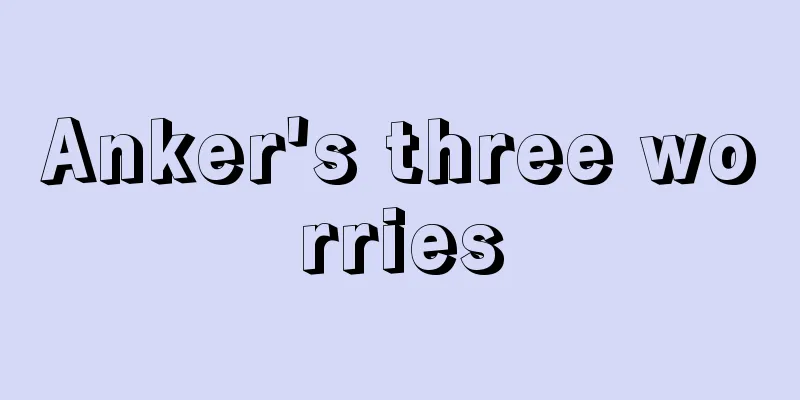

It is another peak season for financial reports. Cross-border sellers at the forefront of the industry have successively disclosed the results of their hard work. Some have seen a sharp increase in revenue and net profit, creating a brilliant performance curve, while others are deeply mired in losses and have difficulty finding a way to grow. As the "number one cross-border seller", Anker Innovations has once again stood out from the crowd and handed in an extremely impressive report card. With annual revenue of over 17.5 billion yuan and a net profit growth rate of over 41%, Anker has maintained steady growth in a market environment full of macro uncertainties. Such performance is undoubtedly outstanding in the entire cross-border industry. However, as an excellent student, Anker has many special troubles behind its glorious appearance. 2023 will still be a year of stability and progress for Anker Innovations. During the reporting period, Anker achieved revenue of 17.507 billion yuan, an increase of 22.85% over the same period last year; net profit attributable to shareholders of the listed company reached 1.615 billion yuan, an increase of 41.22% year-on-year. Throughout 2023, Anker achieved revenue of 16.8 billion in its overseas main battlefield. Among them, the core North American market still occupies a leading position, with annual revenue of about 8.4 billion, accounting for 47.81%. But at the same time , the development of Europe, America, Japan and other regions should not be underestimated, and the proportion of revenue has increased to a certain extent. In terms of sub-categories, during the reporting period, Anker's charging and energy storage products achieved revenue of 8.604 billion yuan, a year-on-year increase of 25.12%; smart innovation products achieved revenue of 4.541 billion yuan, a year-on-year increase of 18.72%; smart audio and video products achieved revenue of 4.285 billion yuan, a year-on-year increase of 26.47%. At first glance, this report card is remarkable. While both revenue and net profit have grown steadily, its profitability has also increased significantly, with a gross profit margin of an astonishing 43.54%, far ahead of its peers. However, the capital market's response was somewhat cold. On April 26, after the financial report was released, Anker's stock price rose by nearly 5%, with a total market value of approximately 34.42 billion yuan. Although Anker's performance has continued to soar since its listing, with its revenue doubling from 9.3 billion yuan in 2020 to 17.5 billion yuan in 2023, its market value has fallen from nearly 80 billion yuan at its peak to less than 40 billion yuan today. When Anker went public in 2020, its P/E ratio was 46.81 times, and at its peak it was as high as 80.75 times. As of April 25, 2024, its P/E ratio has shrunk to around 21.5 times. This reflects, to a certain extent, that investors and shareholders are not too optimistic about the future development prospects of Anker, a top student with outstanding profitability. The fundamental reason is that, under the brilliant performance, Anker still has three development concerns. The domestic market has been difficult to capture In 2023, Anker's overseas revenue accounted for as much as 96.36%, while domestic revenue accounted for only 3.64%. As the growth of overseas markets gradually slows down, the vast development opportunities in the domestic market are expected to provide Anker with a second growth curve. However, despite Anker's increased efforts in domestic business, the brand reputation accumulated overseas has not fed back to domestic development as expected. Therefore, this has also led to a significant decline in investors' expectations for its prospects. Difficult to break free from channel dependence In order to avoid heavy reliance on a single channel, Anker has formulated an "online + offline" omni-channel diversified sales development strategy, and continuously improved its multi-channel and multi-level sales system. But at present, a large part of Anker's revenue still comes from online channels. The financial report shows that in 2023, Anker's online revenue accounted for 70%, while offline revenue accounted for only 29.70%. Among them, Amazon's annual sales revenue accounted for 57.10% of the total revenue. Although the revenue of Anker Innovations' six independent websites increased by 83.87% during the reporting period, it still only accounts for a small part of the overall operating income. More importantly, the characteristics of consumer electronic products, such as fast iteration cycle and low repurchase rate, also determine that the road to independent websites is still long. Born in power bank, confined to power bank Consumer electronics categories are born and die quickly, and it is difficult to establish sufficiently deep technical barriers. Faced with increasingly fierce competitive pressure, Anker chose to take root in the shallow sea strategy, that is, to focus on shallow sea categories that have both market demand and are not overheated, and retain a certain amount of innovation space. Anker's main goal is to avoid focusing on a single category and follow a brand path similar to Procter & Gamble, gradually moving from easy-to-control areas to complex areas, and creating a brand with leading value in each category. However, the more categories it has, the more competitive burden it carries. In order to quickly gain a foothold in each category, Anker has invested huge amounts of R&D expenses over a long period of time to build an advantage in the stock competition. In 2023, its annual R&D expenses reached 1.414 billion yuan, but when it was allocated to many subcategories, it was quite inadequate. Therefore, although Anker has successively entered various fields such as sweeping robots, smart security, smart pets, and projectors, it is limited by the competition dilemma of giants in each field, and rarely creates phenomenal products like Anker. To this day, its main charging series products still account for half of its total revenue. Supported by the shallow sea strategy, Anker focuses on sub-categories in the fields of charging energy storage, smart audio and video, and smart innovation. It has successfully built a brand matrix consisting of six major brands including Anker, eufy, soundcore, Nebula, AnkerWork, and AnkerMake . 1. Charging energy storage products Mainly Anker brand digital charging devices and related accessories, as well as Anker SOLIX series of home photovoltaic and energy storage products. 2. Intelligent and innovative products Smart innovation categories include eufy smart home and AnkerMake 3D printing product series. 3. Smart audio and video products Smart audio and video products mainly include soundcore brand wireless Bluetooth headsets, wireless Bluetooth speakers and other series of products, Nebula brand laser smart projector series of products, and AnkerWork brand wireless Bluetooth microphones, conference cameras and other series of products. It can be seen that the above three product lines together form a huge trunk. Currently, Anker, eufy and soundcore have all grown into leading brands with annual revenue exceeding 3 billion. However, as competition in the industry intensifies, facing the rapid growth and death of consumer electronics and the weakening of shallow-sea dividends, in order to avoid premature decline, Anker chose to continue to expand its track, and continued to branch out on the basis of these three major product lines, extending to rich and diverse categories. While deepening its core business, Anker continues to invest in new energy fields such as portable energy storage and household electric vehicles. In September last year, Anker issued a convertible bond of 1.105 billion yuan to expand the product research and development of new businesses such as portable energy storage and 3D printers, as well as the development and upgrading of multiple industrialization projects. In 2023, based on its past portable energy storage products, Anker successfully launched the consumer-grade new energy brand series Anker SOLIX, and successively launched a number of star products, such as the ultra-long-life balcony photovoltaic energy storage product AnkerSOLIX Solarbank E1600, and the first Anker SOLIX F3800 outdoor power supply that can achieve AC coupling and grid-connected photovoltaic linkage. In order to further realize its multi-brand and multi-channel ambitions, Anker has also invested in a large number of potential brands from different tracks, including home furnishing brand Zhiou Technology, smart hardware brand Zhiyan Technology, and robot brand KeKe Technology. It can be seen that Anker tried to tear off the single label of "power bank brand" by creating more competitive products. However, in the process of aggressive expansion, Anker also encountered many setbacks. At the beginning of this year, Anker Innovations issued a letter to all employees announcing that from January 8, 2024, the team of Mach, the company's high-end smart home brand, will be integrated into other teams of the company, and some members will leave due to personal wishes. It is reported that the Ankermach team was founded in 2021 and mainly deals in household cleaning products such as cordless steam floor cleaners, mopping robots, and vacuuming and sweeping robots. But as we all know, the field of household cleaning is full of strong competitors, such as Ecovacs and Roborock, and compared with the 3C industry, which is fast-growing and fast-dying, it is more challenging to develop and innovate, as well as to have the endurance to cultivate for a long time. Faced with the current situation that the return is less than expected after three years of R&D investment of 300 million, Anker had to let go in time. This is a small microcosm of the hidden dangers exposed on the road of Anker's brand expansion: lack of ecological matrix, dilution of R&D expenses and dragging down the profits of the main brands. To this end, after a series of drastic expansions, Anker realized that many of its product lines had encountered development bottlenecks and lacked competitive barriers, making it difficult to compete with unicorns in their respective tracks. To this end, Anker made a decisive move to adjust its strategy: it began to cut product lines. Public information shows that Anker closed 10 product teams in 2022, including lawn mower robots, handheld cleaning equipment, electric bicycles, etc., and more than 200 employees were affected. After a series of strategic reforms, in 2023, Anker, supported by 17 product categories, delivered a brilliant annual revenue of 17.5 billion and a net profit of 1.6 billion. But for Anker at this stage, there is still a long way to go. With the disappearance of category dividends and channel dividends, Anker's growth rate is also unable to hide its fatigue. On the one hand, the rich product categories that have been expanded have not yet grown to the status of Anker, and they face fierce ecological competition in their respective tracks; on the other hand, third-party platform channels are becoming more and more popular, and there is an urgent need to deepen the diversified channel layout and reduce dependence on a single platform. In such a dilemma, for Anker, which adheres to long-term branding, it is difficult to sit back and relax even with an annual revenue of nearly 20 billion. Faced with a huge product matrix, how to make choices is a profound and complex problem.

|