Anker is also worried after earning 7 billion in half a year

|

If cross-border e-commerce also has a hot word plaza, then "branding" will definitely firmly occupy the most prominent center.

The transformation from a volume-based OEM strategy to a refined branding route has been the mainstream in the industry in recent years. However, there are also differences between brand models. Some grow freely in the private ecosystem of independent sites, while others take root in the public soil of third-party platforms. The most representative cases are undoubtedly SHEIN for the former and Anker for the latter.

The two companies resolutely embarked on completely different tracks at the beginning of their birth, but they were chasing the same brand finish line. Therefore, they both encountered a transformation bottleneck after halfway through their rapid growth. The growth of SHEIN's fast fashion brand business slowed down, and it gradually turned to platformization to explore new growth points; and behind Anker's gorgeous performance curve, it was also trapped in the anxiety that its moat was not strong enough.

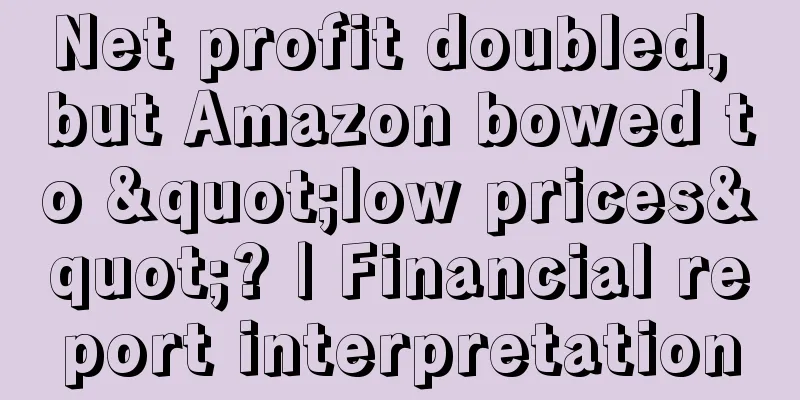

When a number of top sellers disclosed their overseas results in the first half of the year, Anker Innovations, a "heavyweight player", finally made its debut: during the reporting period, it achieved revenue of 7.066 billion yuan, an increase of 20.01% over the same period last year; the net profit attributable to shareholders of the listed company was 820 million yuan, a year-on-year increase of 42.33%.

In 2021, Anker turned the tide amid the wave of account bans and broke through the 10 billion yuan annual revenue mark for the first time. It seems like just yesterday. Now, in just half a year, it has achieved over 7 billion yuan in revenue. Its soaring performance is truly amazing.

Among the series of gorgeous figures, Anker's independent station business shines brightly - it achieved revenue of 456 million yuan in the first half of the year, a year-on-year increase of 112.59%, surpassing the third-party platform business except Amazon. Although its size is only the tip of the iceberg in Anker's business empire, as the fastest growing business at this stage, its development potential is unstoppable.

▲ The picture comes from Anker Innovations report The reason why we focus on the independent station business, which accounts for only 6.46% of the volume, may be traced back to the 3C accessories industry and start with Anker's history of success.

A common consensus among those who travel across borders is that low prices, low frequencies, and rapid growth and rapid death are the indelible legacy of consumer electronics. Another expert once said, "If Huaqiangbei sneezes, the electronics market across the country will catch a cold."

Faced with such a track with frequent iterations and a short life cycle, the earliest batch of gold diggers born in Huaqiangbei all believed in short-termism of making quick money: OEM and low-price internal circulation.

Among the majority of Huaqiangbei brands that rely on cheap supply chains to increase sales, Anker is a relatively special outlier. In an era when counterfeits were rampant and white-label products were prevalent, Anker had long developed the value of brand long-termism. A key step in putting it into practice was to take root in Amazon, a land that contains huge amounts of traffic nutrients.

Initially, Anker relied on OEM sales on Amazon to explore and dig deeper into product categories, gradually creating the prototype of the Anker brand. As the iPhone 4 ushered in a new era of smartphones, Anker quickly found a field that it could master - charging accessories.

This is actually a category with low technical barriers and lack of premium space. However, when the price war in the same category on Amazon was bloody, Anker had already used SEO algorithms to cleverly grab traffic; when most competitors were still at the stage of reselling Huaqiangbei products, Anker had already started the self-development mode and built product competitive barriers.

Such a brand with excellent quality and deep product strength has naturally been "favored" by Amazon. It is also because of the platform support, Apple's endorsement and most importantly its own product advantages that Anker has successfully left other Amazon competitors far behind and become a benchmark brand.

Facts have proved that Anker's brand strategy is very forward-looking. When a group of 3C sellers from Huaqiangbei became rich overnight by selling in large quantities, the gears of fate began to turn, until the account ban wave broke out in 2021, the world line was recovered, and finally swallowed the bitter fruit. However, Anker, which has a brand moat, remained unmoved in the storm of large-scale account bans.

But this does not mean that Anker can sit back and relax. The suspension of its account has made it more deeply aware of the need to get rid of its dependence on Amazon. As the number of sellers on the platform has skyrocketed, the strings in Amazon's hands have been tightened.

Deep bundling with the same platform means higher risks. One wrong move can lead to a complete loss. The previous experience of account suspension has already made this clear. Another important reason is that Anker's goal is to become a global brand, so it is naturally unwilling to be limited to the small online space of Amazon.

To this end, Anker's third-party platform positions have expanded from Amazon to eBay, Walmart and other e-commerce platforms, and sales channels have extended from online to offline. But this is far from enough. Mastering the brand discourse power and accumulating the private domain traffic ecology is the path that Anker must take to implement the spirit of long-termism.

Judging from Anker's latest financial report, its dependence on Amazon is gradually weakening. As of the first half of the year, Amazon's sales revenue accounted for 55.87% of its total revenue. Correspondingly, its independent website business is in a period of rapid growth. Such changes are a positive signal for Anker's brand strategy layout.

Behind the gorgeous revenue curve, Anker also has its own development anxiety. Getting rid of Amazon's dependence and investing heavily in independent websites is certainly its strategic focus and a major hurdle that needs to be broken through, but this anxiety actually comes more from the category itself.

Anker founder Yang Meng has repeatedly emphasized a "shallow sea theory": if consumer electronics is regarded as a vast ocean, then most categories will be concentrated in the shallow sea area, and a few will be located in the deep sea area. Low-priced and low-frequency categories such as charging accessories and Bluetooth headsets are in the shallow sea, while high-priced and high-barrier products such as mobile phones and computers belong to the latter.

From the early days of its overseas expansion, Anker firmly chose the high-risk and high-difficulty path of branding, but it was also very self-aware to avoid head-on confrontation in the deep sea and enter the shallow water categories that are easier to control - where there is market demand but it is not overheated, leaving a certain amount of room for innovation.

Obviously, Anker's logic is, first, to be earlier, to be the first to nurture the brand prototype at the stage when the market lacks brand concepts; second, to be better, to tear off the label of low price and low quality by relying on excellent quality and leading technology; third, to be faster, the low technological barrier characteristics of shallow water categories also mean that it is easy to attack but difficult to defend. Only by always being one step ahead can it avoid the premium space being encroached upon and defend the only ecological niche.

However, Anker's anxiety also comes from this. Shallow sea categories cannot escape the same ceiling from top to bottom, and even if they are ranked first, they cannot rest easy. A more intuitive example is that as the first charging brand in the industry to use gallium nitride technology, Anker successfully created a series of benchmark hits, but this technology was soon conquered by its peers.

To this end, Anker refuses to be tied to a single category. As its founder said in an interview, its brand strategy imitates Procter & Gamble , gradually climbing from easy-to-control areas to complex areas, and creating a brand with leading value in each category.

This strategy was implemented in 2015. Today, Anker's tentacles have extended from charging to multiple fields such as smart innovation and wireless audio, forming a global brand matrix consisting of six major brands: Anker, soundcore, eufy, Nebula, AnkerWork, and AnkerMake.

Judging from Anker's first half report, charging products are still its core source of income, accounting for half of the total revenue. Smart innovation and wireless audio categories account for 27.54% and 22.12% respectively. Overall, its dependence on its main charging category is weakening year by year.

▲ The picture comes from Anker Innovations report However, as mentioned above, Anker's goal is to create a leading brand in each market. When mentioning Anker, the first thing that comes to mind is often the power bank label. When talking about Amazon's top charging brand, Anker is also on the list.

At present, Anker has successively entered into a wide range of fields such as sweeping robots, smart security, smart pets, projectors, etc., and some of them have become leaders, but it has never been able to replicate the same phenomenal explosive products as Anker.

For example, in the field of smart cleaning, Anker's sweeping robot brand has experienced a process from being second only to the foreign leader iRobot to being overtaken step by step by domestic overseas brands such as Ecovacs and Stone Technology.

There is never a shortage of small giants that focus on deep cultivation in various sub-sectors of the shallow sea area. Anker continues to explore and deploy new smart hardware categories, and madly increases investment in the leaders of many potential tracks, attempting to form a series of market-competitive flagship product matrices and become not only a global leader in the power bank category, but also in the consumer electronics industry.

In order to achieve this goal, Anker is very good at leveraging its leading advantages: its brand power and channel competitiveness cultivated over the years, while it is also well aware of the shortcomings of its back-end R&D modules.

Anker also has a clear strategic direction: first, it will continue to focus on key strategic categories on the basis of developing advantageous categories. Its key categories have been adjusted from 20-30 to more than 10; second, it will break free from the constraints of downstream sales and upstream supply. The former means reducing the risk of Amazon's stranglehold, and the latter means getting rid of dependence on suppliers and improving front-end research and development capabilities.

Judging from Anker's first half report, these two strategic policies are currently very effective, but ultimately it will be a long and arduous battle to break through the "demon" in the shallow waters.

Anker's story began in the Amazon and broke out in shallow waters, but there are still more possibilities in deeper waters. Anker, sitting on the throne of power banks, is still looking for its next Anker. |

<<: Brand removals are frequent! New trademark protection cases may affect 3C category sellers

>>: Another major revision! Amazon's front-end review section!

Recommend

What is Club Factory? Club Factory Review

ClubFactory is a big data product selection servic...

What is Social Media Promo Code? Social Media Promo Code Review

Social Media Promo Code is a new form of promotion...

The difficulty of opening a store on Amazon has increased. Will video verification become widely popular?

Amazon has been making frequent moves during this ...

What is Tianhe Wanxiang? Tianhe Wanxiang Review

Shenzhen Tianhe Wanxiang Network Technology Co., L...

Why are there no orders for new products even after advertising?

I recently saw a post like this in the forum: A n...

Amazon’s risk control has been upgraded! Stores that promote products outside the site are also blocked, and the demotion strike is coming again?

▲ Video account focuses on cross-border navigation...

Beware! Amazon has stepped up inspections on refurbished products. How can sellers save themselves?

Recently, Amazon's crackdown measures have bec...

Amazon Advertising Case Study (I)

Q: I’m currently working on a product in a certai...

What is Forest International Freight? Forest International Freight Review

Forest Shipping Co., Ltd. was established in 2010....

Attention! Starting from April, FBA freight rates will rise again! Major shipping companies have begun to adjust freight rates and various surcharges...

As we enter the post-epidemic era, countries have ...

Block the borders of 26 countries! Just now, Europe officially announced...

The international epidemic situation is becoming i...

Costco announces December 2022 results! E-commerce sales fell 6.4% year-on-year!

According to foreign media reports, Costco, a Nort...

It’s all tricks! Summary of Amazon’s daily operation skills

This article mainly shares some sales skills and ...

Cross-border e-commerce tools inventory: 22 best free video editors

Many e-commerce sellers know that high-quality vid...

What is VanTop? VanTop Review

VanTop Technology was founded in September 2017. I...