|

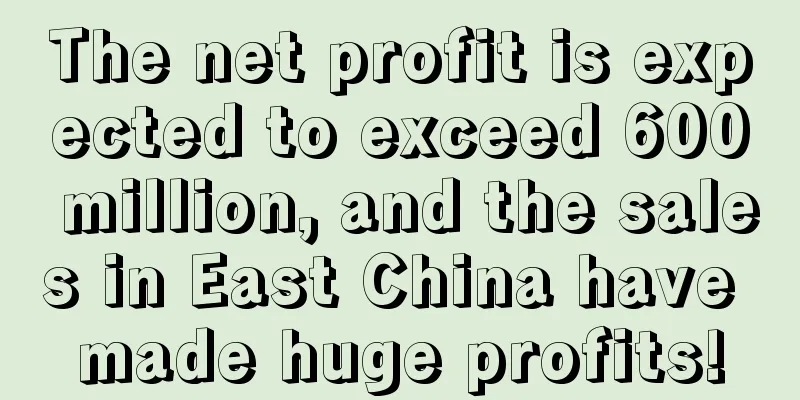

On January 26, the Ministry of Commerce reiterated at a press conference that cross-border e-commerce is one of the new drivers of foreign trade. According to preliminary statistics, there are now 645,000 companies in China with foreign trade import and export performance, of which more than 100,000 are cross-border e-commerce entities. It can be seen that against the backdrop of a sluggish global economic recovery, my country's cross-border e-commerce industry has still demonstrated considerable market vitality and growth resilience. The 2023 report cards recently submitted by cross-border sellers also intuitively reflect this point. It is learned that recently, the cross-border retail giant Jihong Co., Ltd. released its 2023 performance forecast . During the reporting period, Jihong Co., Ltd. expects to achieve a net profit attributable to shareholders of listed companies of 331 million yuan to 368 million yuan, an increase of 80% to 100% over the same period last year . The net profit after deducting non-recurring gains and losses will reach 302 million yuan to 339 million yuan, an increase of 78.46% to 100.19% over the same period last year. The full-year operating performance is expected to increase in the same direction. ▲ The picture comes from Jihong Shares' 2023 performance forecast Affected by inflationary pressure and geopolitical conflicts, the global economy will show a "weak recovery" trend in 2023. Not only is the economic growth momentum insufficient, but the cross-border e-commerce industry is also in constant turmoil. Under the constraints of rising costs, performance pressure and other factors, cost reduction and efficiency improvement have become the main theme of operations. Under this situation, Jihong Co., Ltd. adheres to the digital-driven strategy of "data-based, technology-driven" , continues to increase R&D investment, and iteratively upgrades its independently developed cross-border social e-commerce operation and management system, thereby further promoting performance improvement. It is understood that since the layout of its cross-border e-commerce business in 2017, Jihong Co., Ltd. has invested a total of more than 150 million yuan in research and development expenses to continuously iterate and upgrade its independently developed cross-border social e-commerce operation and management system. At the same time, Jihong shares also continuously practiced innovation empowerment and continuously improved operational management efficiency, so that inventory continued to run at a low level , avoiding the pitfall of performance being dragged down by unsalable inventory due to incorrect prediction of sales trends. At present, the proportion of Jihong shares' cross-border e-commerce inventory to its operating income remains within 3% . In addition, it is worth noting that when the AI wave swept the cross-border industry in 2023, Jihong Co., Ltd. quickly combined it with the company's multiple cross-border e-commerce businesses and achieved many outstanding results, which also played a significant role in promoting its performance growth. In the future, with the further deepening of digital operations and innovation-driven strategies, Jihong Co., Ltd.'s risk resistance may be further enhanced, promoting further growth in performance. It is learned that recently, the cross-border big-name company Lechuang Holdings released its 2023 performance forecast. During the reporting period, Lechuang Holdings expects to achieve a net profit attributable to shareholders of the listed company of 610 million yuan to 650 million yuan, an increase of 178.88% to 197.17% over the same period last year . The net profit after deducting non-recurring gains and losses will reach 230 million yuan to 250 million yuan, an increase of 121.26% to 140.50% over the same period last year. The full-year performance is expected to increase in the same direction. ▲ The picture comes from Lechuang Holdings' 2023 performance forecast As for the reasons for the performance growth in 2023, in addition to the improvement of external unfavorable factors affecting net profit such as the decline in shipping costs and the improvement of exchange rates , Legao Holdings pointed out that it was mainly due to the dual-wheel drive of the company's two core businesses-smart home business and overseas warehouse business. With the development of IoT and AI technologies, as well as the promotion and application of 5G, global consumers' demand for smart home products is increasing day by day. According to a report by TechInsights, global consumers' smart home-related spending is expected to recover in 2023, reaching US$131 billion, a year-on-year increase of 10% . As a well-known brand in the smart home industry, Lejia Holdings maintained steady growth in its own brand business in 2023: benefiting from the increased market penetration of height-adjustable tables and the long-term accumulation of its own brands, brand dividends continued to emerge. At the same time, as the penetration rate of e-commerce in the United States continues to increase and the trend of Chinese cross-border e-commerce brands going overseas continues to strengthen, the demand for overseas warehouses has increased significantly. Legao's overseas warehouse business has also achieved rapid growth: it has served more than 600 overseas companies in total, the number of shipments has increased significantly year-on-year, and profitability has continued to improve. In summary, with the rapid growth of the company's own business and the continuous advancement of overseas warehouse layout, Legg has gradually formed economies of scale in warehousing and logistics, established deep competitive barriers, and achieved impressive results with net profit expected to surge by nearly 200% year-on-year. Moreover, judging from its forward-looking development strategy, it still has considerable development potential in the future. What do you think about this? Welcome to discuss in the comment area~

|